Macro Intelligence

Ghana's Exchange-Rate Pass-Through: How Cedi Depreciation Feeds into Consumer Inflation

An empirical analysis of how cedi depreciation transmits into Ghana's consumer prices, using five decades of monthly data. Headline pass-through is strong in the long run but weak month-to-month; food, housing, and transport effects build over roughly 11 months.

Cedi depreciation is one of the strongest drivers of Ghanaian inflation. This report quantifies the exchange-rate pass-through into consumer prices, overall and by category, and the lag at which it operates.

Ghana’s Exchange-Rate Pass-Through: How Cedi Depreciation Feeds into Consumer Inflation

How quickly a weaker cedi feeds into prices, where the pressure lands first, and what the next 12 months imply for businesses, investors, and policymakers.

Published: 2026-06-28 | KANA AI Research

Executive Summary

Ghana’s inflation is tied to the exchange rate, but not in a simple, one-for-one way. Drawing on the Ghana Statistical Service’s long monthly interbank cedi-dollar series and monthly CPI data from the IMF and the Ghana Statistical Service, the central result is clear: cedi depreciation shapes the inflation trend over the long run far more than it moves any single month’s inflation print. Over the sample from June 1972 to August 2024, the cedi-dollar rate and headline CPI track each other very closely in levels, with a correlation of 0.97 — but that figure mostly reflects the fact that both series trend upward over decades. The more decision-useful measure is the correlation in monthly changes, which is just 0.17: positive and statistically significant, but modest. A weaker cedi does push inflation higher, in other words, but it is only one driver among several.

Timing matters as much as magnitude. The lead-lag analysis shows that cedi depreciation reaches consumer prices most strongly after roughly 11 to 12 months. That fits Ghana’s inflation structure: imported final goods reprice relatively quickly, fuel and transport costs transmit through logistics chains, utility tariffs move on review cycles, and second-round effects then spread into food and services. The category evidence points the same way — food, housing, and transport all show weak month-to-month co-movement with the exchange rate, yet their strongest association also arrives around a 12-month lag.

For the near term, the inflation outlook remains upward-sloping. Using Ghana Statistical Service monthly CPI through January 2026, the 12-month forecast lifts the index from 262.3 to 281.2 by January 2027 — a 7.2% rise. That is an index forecast rather than a direct inflation-rate forecast, but it implies that disinflation will be fragile if the cedi weakens again. One honest caveat frames the currency side: the deep interbank cedi-dollar series runs only through August 2024, when it stood at 15.1 cedi per US dollar. That series is the right basis for the historical econometrics because it is deep, but it is not current enough to anchor a decision-grade 12-month exchange-rate forecast from a 2026 starting point — so this report does not present one.

Key findings:

- Headline CPI and the interbank cedi-dollar rate have a 0.97 correlation in levels over June 1972–August 2024, but the more meaningful correlation in monthly changes is only 0.17. That means persistent depreciation matters; month-to-month inflation is not dominated by FX alone.

- The strongest lead-lag relationship appears at 11–12 months, with peak cross-correlation around 0.979 at an 11-month lag. The inflation effect of depreciation is gradual and peaks about a year later.

- Granger-causality tests with 12 monthly lags show bidirectional predictive power at the 1% level. Past exchange-rate changes help forecast CPI, and past CPI changes also help forecast the exchange rate; this is predictive precedence, not structural causation.

- Across food, housing, and transport, first-difference correlation is weak at 0.044, while peak cross-correlation reaches only about 0.40 at a 12-month lag. Category pass-through exists, but it is slow and uneven rather than immediate.

- The CPI forecast rises from 262.3 in January 2026 to 281.2 in January 2027, a 7.2% increase. The forecast band for January 2027 is 257.9 to 312.0, showing a clear upward path but still meaningful uncertainty around the pace.

1. How Exchange-Rate Pass-Through Works in Ghana

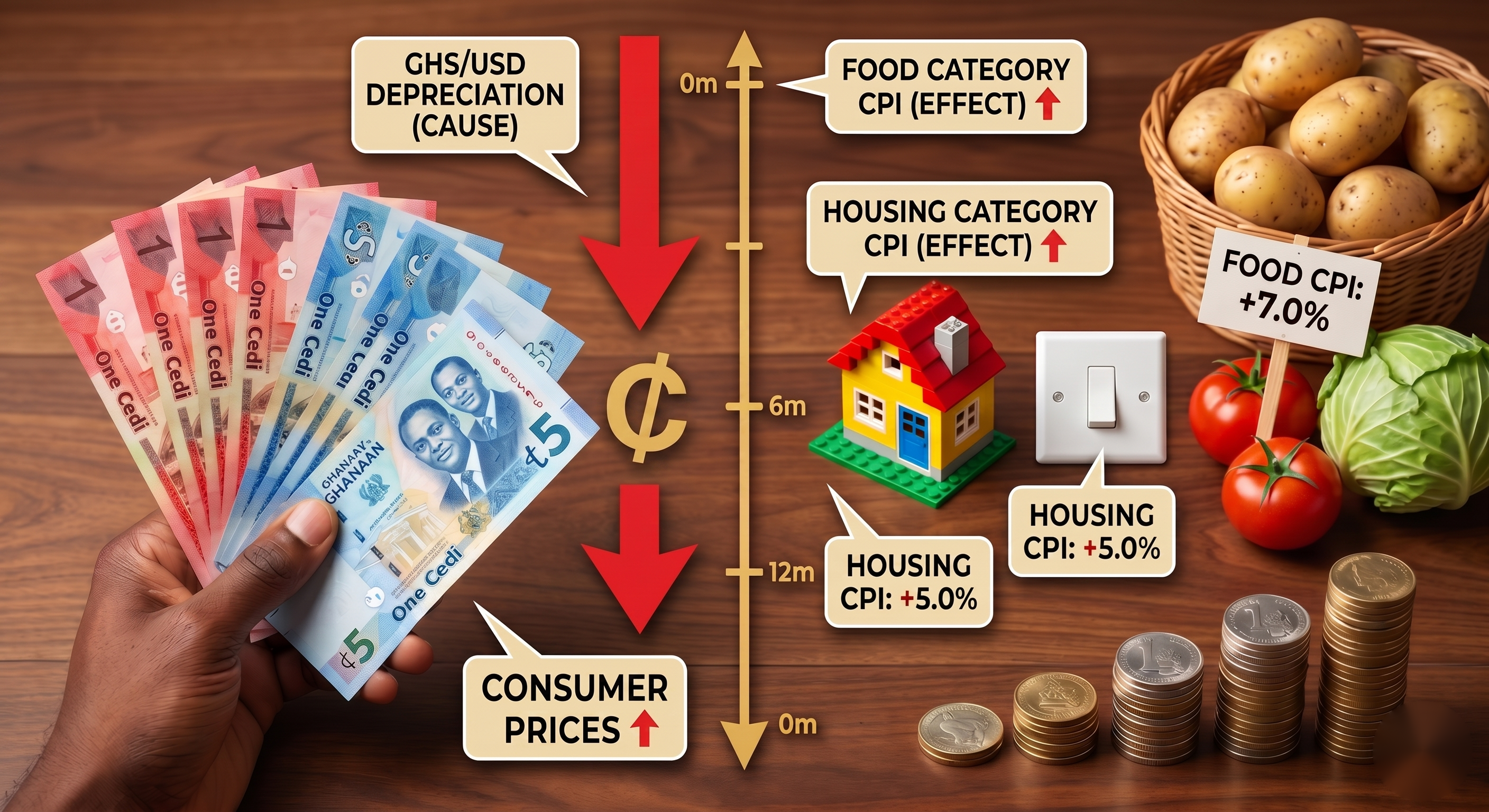

Exchange-rate pass-through is the extent to which a change in the cedi-dollar rate feeds into domestic prices. In Ghana, theory predicts meaningful pass-through because the consumption basket contains a large imported component and because several high-weight categories are either directly import-intensive or indirectly exposed through fuel, transport, and utility costs.

Four channels matter most.

First, imported final goods become more expensive in cedi terms when the currency weakens. This is the fastest and cleanest transmission route, especially where local substitutes are limited.

Second, fuel and transport amplify the shock. Ghana’s import bill is large, and imported petroleum products are a central transmission mechanism into non-food inflation and then into economy-wide logistics costs.

Third, utility tariffs transmit depreciation with a regulatory lag. The Public Utilities Regulatory Commission explicitly notes that tariff reviews reflect the exchange rate underpinning the prior adjustment cycle. That means the housing-related CPI basket can react later than tradable goods, but once tariffs move, the effect is broad-based because utilities are inputs into households and firms alike.

Fourth, second-round effects matter. Once imported goods, fuel, and utilities rise, food distribution, services pricing, wage bargaining, and inflation expectations begin to adjust. This is why the strongest statistical relationship appears with a lag rather than in the same month.

What this means: Ghana does not import inflation only through supermarket shelves. It imports inflation through the full cost structure of the economy: fuel, freight, utilities, and expectations. That is why a currency shock can keep feeding inflation long after the initial depreciation.

2. Historical Context: Why the Timing Is Slow but Persistent

Ghana’s recent macro history helps explain the empirical pattern. Official budget documents describe intense foreign-exchange pressure and significant cedi weakening during stress episodes, alongside policy efforts to stabilize inflation and the exchange rate. Banking-sector and macroeconomic commentary likewise describes periods of sharp inflation volatility linked to fiscal imbalances, exchange-rate weakness, and tighter financial conditions.

The long-run data also show a structural shift around late 2016. Structural-break tests identify a break in the exchange-rate series in December 2016 and in CPI in November 2016. That aligns with a period of macro stress and a change in the inflation-exchange-rate relationship. The broader policy narrative then intensifies again in the 2022–2023 episode, when exchange-rate volatility and inflation pressures became central macroeconomic risks.

As Figure 1 shows, the cedi-dollar rate and CPI both trend upward strongly over time, but not in lockstep month by month.

Figure 1. Ghana Interbank Cedi-Dollar Rate and Consumer Price Index (Dual Axis)

What this means: Ghana’s inflation regime is not static. Pass-through becomes more visible in stress periods, when depreciation is large enough to overwhelm pricing buffers, subsidies, and inventory smoothing.

3. Empirical Results

3.1 Headline CPI: Short-Run Association and Long-Run Link

Using monthly headline CPI and the interbank cedi-dollar rate over their longest common window, June 1972 to August 2024 (), the headline result is a sharp contrast between long-run co-movement and short-run noise.

Table 1 summarizes the core headline tests.

Table 1. Headline exchange-rate pass-through into Ghana CPI

| Test | Variables | Sample | Result | Plain-language reading |

|---|---|---|---|---|

| Levels correlation | CPI level and interbank USD/GHS level | Jun 1972–Aug 2024, n=627 | 0.97 | Very strong long-run co-movement, but largely driven by common trends |

| First-difference correlation | Monthly change in CPI and monthly change in USD/GHS | Jun 1972–Aug 2024, n=627 | 0.17 | Weak but statistically significant short-run association |

| Cointegration (Engle-Granger) | CPI level and interbank USD/GHS level | Jun 1972–Aug 2024, n=627 | Test statistic = -4.36; p = 0.002 | Suggests a long-run relationship, though it should be treated as indicative |

| Structural break | CPI and USD/GHS relationship | Long monthly sample | Nov–Dec 2016 break | Pass-through regime changed around the 2016 stress episode |

Source:

The cointegration result means the two series appear to move together over the long run rather than drifting apart indefinitely. But this is not a clean textbook case: both series are highly persistent — in technical terms, integrated of order two rather than one — which weakens a formal cointegration reading. The long-run link is therefore best treated as directional rather than as a precise structural estimate.

What this means: If the cedi weakens for a few weeks, do not expect headline inflation to jump one-for-one. If the cedi weakens persistently over quarters, higher inflation becomes much harder to avoid.

3.2 Lead-Lag Structure: When Pass-Through Hits Hardest

The lead-lag evidence is the most actionable part of the analysis. Cross-correlation between exchange-rate changes and inflation shows the strongest association when exchange-rate changes lead CPI by 11 to 12 months, with the peak at 11 months.

This can be written schematically as:

where is the monthly change in the interbank cedi-dollar rate and is the monthly change in CPI months later.

Table 2 sets out the lead-lag and predictive results.

Table 2. Lead-lag and predictive relationship between the cedi and headline CPI

| Test | Specification | Sample | Result | Interpretation |

|---|---|---|---|---|

| Cross-correlation | Monthly change in the cedi rate against the monthly change in CPI, tested at lags of 0 to 12 months | Jun 1972–Aug 2024, n=627 | Peak at lag 11; coefficient 0.979 | Depreciation is most strongly associated with higher CPI about 11 months later |

| Granger causality | CPI change regressed on its own 12 lags plus 12 lags of the cedi change; joint significance of the cedi-change terms | Jun 1972–Aug 2024 | F = 25.09; p < 0.001 | Past exchange-rate changes help forecast CPI |

| Reverse Granger causality | Cedi change regressed on its own 12 lags plus 12 lags of CPI change; joint significance of the CPI-change terms | Jun 1972–Aug 2024 | F = 52.28; p < 0.001 | Past CPI changes also help forecast the exchange rate |

Source:

The Granger result should be read carefully. It supports a predictive statement: past exchange-rate moves contain information about future inflation, and past inflation contains information about future exchange-rate moves. It does not prove that one structurally causes the other. The reported VAR underpinning this test is unstable, so the result is directional rather than a basis for precise policy calibration.

What this means: For budgeting and pricing, Ghanaian firms should think in quarters, not weeks. The main inflation hit from a depreciation shock tends to arrive over the following year, not only in the month of the shock.

3.3 Category-Level Pass-Through: Food, Housing, and Transport

Drawing on Ghana Statistical Service monthly CPI by category over 1998–2026 and the interbank cedi-dollar series, category-level pass-through is present but weaker than headline intuition often suggests.

As Figure 2 shows, category CPI paths diverge meaningfully over time, reflecting different import content, tariff structures, and administered-price dynamics.

Figure 2. Ghana Consumer Price Index by Spending Category, 1998-2026

Across the three requested categories — food; housing, water, electricity, gas and other fuels; and transport — the short-run pattern is consistent rather than differentiated. The estimates did not separate the categories into materially different short-run coefficients in this sample, so the result is best read as a shared, lagged transmission pattern rather than a ranking of which category is most exchange-rate-sensitive.

Table 3. Exchange-rate pass-through for food, housing, and transport CPI (combined)

| Measure | Value |

|---|---|

| Sample | 1998–2025, monthly (n = 748) |

| Correlation in monthly changes | ≈ 0.04 (weak) |

| Peak cross-correlation | ≈ 0.40, at a 12-month lag |

| Granger: exchange rate → category CPI | F = 3.49; p = 0.0001 (significant) |

| Granger: category CPI → exchange rate | F = 1.55; p = 0.10 (not significant) |

Source:

The category-level Granger test uses the same predictive framework as the headline analysis:

where is the CPI index for food, housing, or transport. The direction is clear: exchange-rate changes carry useful forward information for these categories, while the categories do not meaningfully predict the cedi in return.

Theory helps explain why the measured short-run correlations are weak even where economic exposure is obvious. Food prices are affected by imported staples and processed foods, but also by domestic harvests and distribution conditions. Housing reacts through imported materials and utility tariffs, but those adjustments often occur on a review cycle rather than continuously. Transport is highly exposed through fuel and spare parts, but administered pricing can create stepwise jumps rather than smooth monthly transmission.

What this means: Importers and retailers should not expect a clean, immediate pass-through coefficient by category. Food, housing, and transport all absorb FX pressure, but the timing is staggered and mediated by regulation, inventories, and domestic cost conditions.

3.4 Regional Dispersion: Where Inflation Has Run Hottest Since 2021

The regional CPI panel is not central to the exchange-rate econometrics, but it shows that price pressure has not been spread evenly across Ghana. One point of interpretation matters first: these are CPI index levels rebased so that 2021 equals 100, so a higher reading means prices in that region have risen more since 2021, not that the region is more expensive in absolute terms. On that basis, the Eastern Region has seen the most cumulative inflation, with a latest index of 305.5 — roughly three times its 2021 level — followed by North East at 292.9 and Western North at 278.3. Oti, at 234.3, has seen the least.

Figure 3. Ghana Consumer Price Index by Region, Latest Reading (2021 = 100)

The spread is meaningful but not extreme. Eastern's index sits about 30% above Oti's (305.5 versus 234.3), which means prices in the hottest region have risen roughly 30% more since 2021 than in the coolest. Pass-through is a national shock, but its accumulated effect on the price level has clearly varied by region.

What this means: Exchange-rate pass-through does not land on a uniform national price surface. Firms with regional distribution networks should expect different pricing pressure across markets, even when the national FX shock is the same.

4. Forward-Looking Outlook

The strongest forward-looking result in the evidence base is the CPI forecast. Using Ghana Statistical Service monthly CPI from January 1998 to January 2026, the 12-month path rises steadily from 262.3 in January 2026 to 281.2 in January 2027. That is a 7.2% increase in the index over 12 months. The forecast interval for January 2027 is 257.9 to 312.0, which is wide enough to matter operationally but still centered on further price increases.

Table 4 presents the monthly forecast path.

Table 4. Twelve-month CPI outlook for Ghana

| Month | Forecast CPI index | Lower bound | Upper bound |

|---|---|---|---|

| 2026-02 | 268.1 | 258.6 | 280.2 |

| 2026-03 | 268.2 | 258.5 | 281.8 |

| 2026-04 | 269.4 | 258.8 | 284.6 |

| 2026-05 | 271.4 | 260.2 | 288.0 |

| 2026-06 | 272.3 | 259.3 | 289.6 |

| 2026-07 | 272.7 | 257.8 | 291.9 |

| 2026-08 | 273.0 | 256.9 | 293.4 |

| 2026-09 | 274.8 | 257.2 | 297.6 |

| 2026-10 | 276.2 | 256.8 | 300.6 |

| 2026-11 | 276.1 | 255.1 | 302.8 |

| 2026-12 | 279.0 | 256.8 | 307.6 |

| 2027-01 | 281.2 | 257.9 | 312.0 |

Source:

The exchange-rate outlook is more constrained. The historical pass-through analysis correctly uses the long interbank cedi-dollar series because depth matters for correlation, lead-lag, and cointegration. But the latest exchange-rate observation in the evidence base is August 2024 at 15.1 cedi per US dollar. That is too stale for a decision-grade 12-month exchange-rate forecast from a 2026 starting point. The right conclusion is therefore narrower: the historical relationship implies that renewed cedi weakness in 2026 would most likely add to inflation pressure through 2027, with the strongest effect arriving over the following 11 to 12 months.

What this means: Asset managers and treasury teams should treat the inflation outlook as still upward-biased. Even without a current exchange-rate forecast base, the historical transmission pattern says that any fresh FX stress today would keep feeding prices well into next year.

Data Sources and Methodology

This report draws on three core monthly datasets. First, headline CPI from the IMF’s International Financial Statistics, used for the long historical headline relationship. Second, the Ghana Statistical Service’s interbank US-dollar exchange-rate series, used as the preferred exchange-rate measure because it provides a deep monthly history for Ghana. Third, Ghana Statistical Service CPI category data, used for food, housing, and transport analysis and for the CPI forecast through January 2026.

The empirical strategy separates short-run from long-run relationships.

- Correlation in levels compares the CPI level and the interbank USD/GHS level over the common monthly window.

- Correlation in first differences compares monthly changes in CPI and monthly changes in the exchange rate, which is the relevant short-run measure when both series trend over time.

- Cross-correlation uses across lags to identify when pass-through is strongest.

- Granger causality estimates whether lagged exchange-rate changes improve forecasts of CPI beyond CPI’s own history, using 12 monthly lags.

- Cointegration tests whether CPI and the exchange rate share a stable long-run relationship in levels.

- Forecasting uses the monthly CPI index through January 2026 to project the next 12 months.

The practical interpretation standard is strict. Correlation means co-movement, not causation. Granger causality means predictive precedence, not structural causation. Cointegration means long-run co-movement, not a fixed pass-through coefficient in every month.

Limitations

Two limitations matter. First, the long exchange-rate series in the evidence base ends in August 2024, so it is the correct series for historical econometrics but not current enough to anchor a 2026 exchange-rate forecast. Second, some long-run specifications are weakened by the order of integration of the series, so the cointegration evidence should be treated as indicative rather than as a precise structural elasticity.

Policy Implications

For Government

The policy message is that exchange-rate stabilization is inflation policy. Because the strongest pass-through arrives after 11 to 12 months, a depreciation shock that is not contained quickly can keep feeding inflation for a full budget cycle. That argues for tighter coordination between fiscal financing, FX liquidity management, and administered-price policy. Utility and fuel pricing should be managed transparently and predictably, because delayed tariff adjustments can compress inflation temporarily only to release it later in larger step changes.

Government should also treat imported inflation as a supply-chain issue, not only a monetary one. Food and transport exposure means port costs, fuel taxes, and logistics bottlenecks can magnify exchange-rate pass-through. A practical response is to prioritize FX access and customs efficiency for high-weight essentials and productive imports rather than allowing broad-based cost escalation.

For Investors

For asset managers, the key insight is that FX weakness is an inflation signal with a long tail. The short-run correlation is modest, but persistent depreciation raises the probability of higher inflation over the following year. That favors shorter-duration fixed-income positioning when the cedi comes under pressure, wider inflation buffers in nominal return targets, and closer monitoring of sectors with regulated-price exposure.

Equity investors should distinguish between firms that can reprice quickly and firms that cannot. Businesses with imported inputs but weak pricing power will see margin compression first. Businesses with strong pricing power or natural FX hedges will absorb the shock better. The 11–12 month transmission window gives investors time to rotate, but not to ignore the signal.

For Development Partners

Development partners should read Ghana’s inflation problem as partly a foreign-exchange transmission problem. Support that improves reserve resilience, trade finance, fuel-supply stability, and utility-sector cost recovery can reduce the inflationary impact of future depreciation episodes. Technical support should also focus on high-frequency monitoring of category-level inflation and administered-price adjustments, because the category evidence shows that transmission is uneven and delayed rather than uniform.

The broader development implication is straightforward: when the cedi weakens, the inflation burden does not stay in the financial system. It moves into food bills, transport fares, utility costs, and eventually household welfare. The transmission is not immediate, but it is persistent.

References

-

Public Utilities Regulatory Commission (Ghana) [link]

-

Customs Revenue in Ghana: Recent Trends and Their Causes — Ministry of Finance, Ghana [link]

-

Statement on Inflation — Ghana Statistical Service [link]

-

2023 Budget Highlights — Ministry of Finance, Ghana [link]

-

SGTS Update (March 2024) — Ministry of Finance, Ghana [link]

-

Ghana 2023 IMF Extended Credit Facility Programme — Ministry of Finance, Ghana [link]

-

Ghana’s Banks Through the Shock — Ghana Association of Banks [link]

-

2025 Budget Speech — Ministry of Finance, Ghana [link]

-

Inflation Dynamics and the Cost of Credit — Ghana Association of Banks [link]

-

2025 Budget Statement and Economic Policy — Ministry of Finance, Ghana [link]

-

COCOBOD Turnaround Strategy — Ministry of Finance, Ghana [link]

Disclaimer. This report is produced by KANA AI for informational and educational purposes only. It does not constitute investment advice, a research recommendation, or an offer or solicitation to buy or sell any security, and it should not be the sole basis for any investment decision. Figures are computed from publicly available data and reported company fundamentals, which may be incomplete, delayed, or contain errors; valuation ratios reflect the latest available data and can lag fast-moving prices. Past performance is not indicative of future results. Readers should conduct their own due diligence and consult a licensed financial adviser. KANA AI accepts no liability for decisions taken on the basis of this report.

Next Step

Want to discuss this research or commission a similar analysis?

KANA AI can produce tailored research reports for your specific market, sector, or investment thesis.