Monetary Policy

Central Bank Policy Transmission: How Rate Decisions Reach the Real Economy Across Four African Markets

Twenty-five years of CPI and interest rate data reveal a stark divergence in monetary policy effectiveness: South Africa operates near-textbook inflation targeting while Ghana and Nigeria face severe transmission breakdowns driven by fiscal dominance and currency instability.

When a central bank changes its policy rate, the decision should ripple through the financial system to affect lending, investment, and inflation. This report examines how effectively that transmission mechanism works across Ghana, Nigeria, Kenya, and South Africa.

Central Bank Policy Transmission

How Rate Decisions Reach the Real Economy Across Four African Markets

Published: May 2026 | KANA AI Research

Executive Summary

When a central bank raises or lowers its policy rate, the decision is supposed to ripple outward through the financial system: banks adjust lending rates, businesses recalibrate investment plans, consumers modify spending, and inflation responds. This is the monetary policy transmission mechanism, and it works reasonably well in advanced economies with deep financial markets and credible institutions.

In Ghana, Nigeria, Kenya, and South Africa, the story is different. This report examines 25 years of data across these four economies to assess how effectively central bank rate decisions transmit to the real economy. The findings reveal a stark divergence: South Africa operates a near-textbook inflation targeting regime, while Ghana and Nigeria face severe transmission breakdowns driven by fiscal dominance, currency instability, and shallow financial markets.

Key findings:

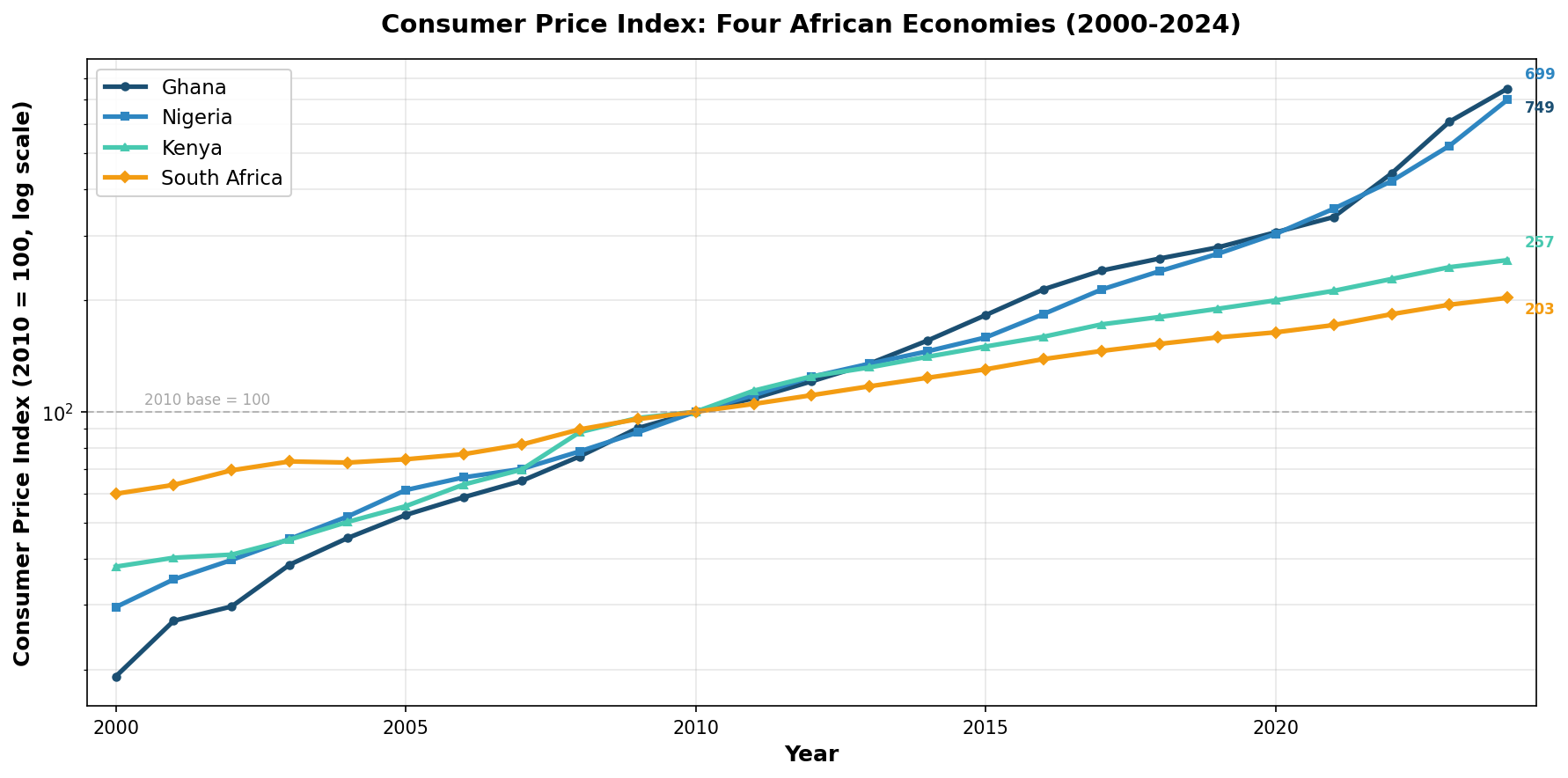

- Inflation divergence is extreme. Ghana's CPI (2010=100) reached 749 by 2024 -- prices 7.5x their 2010 level. Nigeria hit 699 (7x). Kenya reached 257 (2.6x). South Africa stood at 203 (2x) [1]. The gap between the best and worst performers widened from near-parity in 2010 to a 3.7x differential by 2024.

- Real interest rates tell a credibility story. South Africa has maintained consistently positive real rates (averaging 4.3% over 25 years), reflecting SARB's institutional credibility [2]. Nigeria's real rate collapsed to -25.8% in 2019, reflecting a period where the CBN held nominal rates artificially low while inflation surged [3].

- Nigeria's naira float destroyed USD-denominated GDP. The naira moved from ~305/USD in 2020 (the official rate) to 800/USD in 2024 [4], causing Nigeria's nominal GDP in dollar terms to fall 61% from $647B (2022) to $252B (2024), even as real GDP growth continued at 3-4%.

- Ghana's 2022-2025 crisis and recovery demonstrates the limits and potential of monetary policy. Inflation peaked at 54.6% in December 2022, then collapsed to 6.3% by November 2025 following aggressive fiscal consolidation, IMF support, and tight monetary policy [5].

1. The Four Central Banks

Four central banks, four mandates, four levels of institutional credibility. Understanding the transmission problem starts with understanding the institutions.

Bank of Ghana (BoG)

Mandate: Price stability, with a medium-term inflation target of 8 +/- 2 percent [6].

Primary tool: The Monetary Policy Rate (MPR), set by the Monetary Policy Committee.

Credibility challenge: The BoG's credibility suffered severely during the 2022-2023 crisis. Inflation peaked at 54.6% in December 2022, far exceeding the target band [7]. The Cedi depreciated 27.8% against the USD in 2023 alone [8]. A key vulnerability was monetary financing of the budget -- a structural weakness that let fiscal pressures override monetary policy; ending that practice became a core structural benchmark under the 2023 IMF programme [1].

Transmission assessment: Weak to moderate. The BoG's rate decisions transmit slowly to lending rates due to high banking sector concentration, wide interest rate spreads, and the dominance of government securities in bank portfolios. Research from the Ghana Association of Banks found that interest rate movements exert statistically significant but lagged effects on credit quality, with aggressive tightening actually increasing non-performing loans as debt-servicing pressures materialise [9].

Central Bank of Nigeria (CBN)

Mandate: Price stability and exchange rate stability -- a dual mandate that often creates internal contradictions.

Primary tool: The Monetary Policy Rate (MPR). The CBN also deploys the Cash Reserve Ratio (CRR), which has been used aggressively as a sterilisation tool [10].

Credibility challenge: The CBN's credibility was severely damaged during the 2015-2023 period of multiple exchange rate windows and administrative controls. The MPR was raised from 12% (2013) to 13% (2014) [10], then to 16.5% (November 2022) [11], and through a series of 2023 hikes to 18.75% by mid-2023 [3] as inflation accelerated to 26.72%. The combination of high MPR, multiple exchange rate regimes, and capital controls created a system where the policy rate was disconnected from actual market conditions.

Transmission assessment: Weak. The multiple exchange rate regime (which persisted until the June 2023 naira float) meant that the CBN's rate decisions operated in a distorted environment. The spread between the official and parallel market rates at times exceeded 100%, meaning that monetary policy operated on a fictitious price signal [12]. The NDIC has documented the challenges of monetary policy transmission in the context of Nigeria's financial openness [13].

Central Bank of Kenya (CBK)

Mandate: Price stability, formulating and implementing monetary policy to achieve low and stable inflation [14].

Primary tool: The Central Bank Rate (CBR), which forms the base for all monetary policy operations. The CBK also operates an interest rate corridor with a standing lending facility and deposit facility [15].

Credibility track record: The CBK has maintained relatively strong credibility. It raised the CBR from 8.5% (mid-2014) [16] to 10% (June 2015) [17] and then to 11.5% [18] to anchor inflation expectations. More recently, it raised the CBR from 10.5% (July 2023) to 13.0% (February 2024) to address exchange rate pressures [19]. Kenya's CPI trajectory (2.6x since 2010) reflects this relative discipline.

Transmission assessment: Moderate. The CBK's transmission mechanism works through interest rate, credit, exchange rate, and asset price channels [14]. However, effectiveness depends on the stability of the money demand function, and Kenya's expanding financial sector -- including mobile money -- has complicated transmission. Research from the Kenya Bankers Association has examined the risk-taking transmission channel, finding that monetary policy affects bank lending behaviour through risk appetite as well as through the traditional interest rate channel [20].

South African Reserve Bank (SARB)

Mandate: Protect the value of the currency in the interest of balanced and sustainable economic growth. SARB operates a formal inflation targeting framework with a 3-6% target band.

Primary tool: The repo rate. The Monetary Policy Committee maintained the repo rate at 8.25% and the prime rate at 11.75% in March 2024, with annual consumer price inflation at 5.3% [2].

Credibility track record: SARB is widely regarded as the most credible central bank among the four. Its inflation targeting framework, implemented in 2000, has kept inflation within the 3-6% band for most of the past two decades. The Monetary Policy Implementation Framework (MPIF), implemented in 2022, has helped SARB better manage growing structural liquidity while improving policy transmission [21]. The IMF has noted that SARB's transparent practices reinforce the effectiveness of monetary policy.

Transmission assessment: Strong. South Africa has the deepest financial markets, the most developed banking sector, and the most transparent monetary policy framework among the four countries. The government bond yield curve decreased by 40-140 basis points in the period under review, reflecting improved investor confidence [22]. PwC analysis shows the major banks' combined headline earnings reached a record R113.2 billion, underpinned by strong operating franchises [23]. The Banking Association South Africa notes that banks offer each customer an interest rate quoted using prime as a reference rate, directly linked to SARB's repo rate decisions [24].

2. The Inflation Divergence

The CPI data tells the most important story in this report. Using a common base year (2010 = 100), the four countries' price levels have diverged dramatically over 25 years.

CPI Trajectory (2010 = 100)

| Year | Ghana | Nigeria | Kenya | South Africa |

|---|---|---|---|---|

| 2000 | 19.2 | 29.6 | 38.1 | 60.0 |

| 2005 | 52.6 | 61.4 | 55.5 | 74.4 |

| 2010 | 100.0 | 100.0 | 100.0 | 100.0 |

| 2015 | 182.6 | 158.9 | 150.2 | 130.3 |

| 2020 | 306.0 | 302.9 | 200.2 | 164.1 |

| 2024 | 749.3 | 699.4 | 257.4 | 203.4 |

Source: World Bank Development Indicators (FP.CPI.TOTL) via KANA AI Database

What this means: A basket of goods that cost 100 currency units in 2010 now costs 749 units in Ghana and 203 units in South Africa. The gap between the best and worst performers has widened from parity in 2010 — all four are 100 by construction in the base year — to a 3.7x differential by 2024. This is not a story about individual price shocks -- it is a story about the cumulative effect of monetary policy credibility, fiscal discipline, and institutional quality over a quarter century.

Two Clubs

The data reveals two distinct inflation clubs:

High-inflation club (Ghana, Nigeria): Both countries saw their CPI multiply roughly 7x from the 2010 base. This reflects chronic fiscal deficits, exchange rate instability, monetary financing of budgets, and periodic crises. Ghana's acceleration was particularly sharp after 2022, when the Cedi's depreciation of 27.8% against the USD [8] and the post-COVID/Ukraine shock drove inflation to 54% [7].

Moderate-inflation club (Kenya, South Africa): Both countries kept their CPI multiplier below 2.6x. South Africa's 2x reflects the discipline of SARB's inflation targeting regime. Kenya's 2.6x reflects the CBK's relatively effective (if imperfect) monetary policy operations and lower exchange rate volatility.

3. Interest Rate Dynamics

Real interest rates reveal whether credit is actually expensive in real terms, regardless of what the headline policy rate suggests. The series charted here is the World Bank's real interest rate (FR.INR.RINR) — the bank lending rate deflated by the GDP deflator. That is a broader gauge than the simpler policy-rate-minus-CPI measure quoted in a few places below, and the two can diverge sharply, so each is labelled where it matters.

The South Africa Benchmark

South Africa's real interest rate has been consistently positive over the entire 25-year period, averaging approximately 4.3%. The range has been narrow -- from a low of 0.6% (2021, during COVID-era easing) to a high of 8.0% (2003). This consistency is the hallmark of a credible inflation targeting regime: SARB adjusts its nominal repo rate sufficiently to maintain positive real rates, even during global shocks [21].

The latest real lending rate of 7.4% (2024, World Bank series) is at the upper end of the historical range, reflecting SARB's hawkish stance in response to the post-COVID inflation surge. Measured more simply as the repo rate (8.25%) minus headline CPI (5.3%) [2], the real policy rate is a still-clearly-positive ~2.9%. By either gauge, SARB is holding real rates firmly positive while keeping inflation within the 3-6% target band.

Kenya's Steady Band

Kenya's real interest rate has averaged approximately 7.1% over the period, higher than South Africa's. However, it has been more volatile, ranging from -10.1% (2009) to 17.8% (2001). The negative episodes correspond to periods when inflation spiked faster than the CBK could raise rates -- notably during the 2008 food crisis and the 2011 drought. The latest reading of 7.75% (2023) reflects the CBK's tightening cycle in response to exchange rate pressures.

The Nigeria Anomaly

Nigeria's real interest rate tells the most dramatic story. The -25.8% reading in 2019 (World Bank series) is an extreme outlier. It partly reflects how that series is constructed — the bank lending rate deflated by the GDP deflator — in a year when deflator inflation ran well above nominal lending rates. The broader point holds on any measure: with the CBN holding the MPR at 13.5% against double-digit inflation and a heavily managed exchange rate, real returns to lending were deeply negative.

On the same World Bank series, the real lending rate recovered to +2.88% (2023). That measure is positive, but it sits awkwardly against the policy stance: with the MPR at 18.75% and headline inflation at 26.72%, the policy-rate-minus-CPI gap was about −8% — deeply negative [3]. That divergence between the two gauges, plus the difficulty of measuring true inflation in an economy still adjusting to the June 2023 naira float, is exactly why Nigeria's real-rate picture must be read with care.

Ghana: The Missing Data

Ghana's real interest rate data is not available in the KANA database for the study period. This is itself informative -- during the 2022-2023 crisis, with inflation at 54% and the policy rate at approximately 30%, the real rate was deeply negative. By 2025, with inflation at 6.3% and treasury bill rates at approximately 11% [5], Ghana had achieved positive real rates for the first time in years -- a key milestone in the recovery.

4. The Transmission Problem

The gap between a central bank's rate decision and its effect on the real economy is where transmission succeeds or fails. Five channels carry monetary policy to the real economy: the interest rate channel, the credit channel, the exchange rate channel, the asset price channel, and the expectations channel. In each of the four countries, these channels operate with different efficiency.

Why Transmission Fails in West Africa

Shallow financial markets. In Ghana and Nigeria, a large share of economic activity occurs outside the formal banking system. Informal markets, cash-based transactions, and limited financial inclusion mean that rate changes affect only the portion of the economy that interacts with the formal financial system.

Fiscal dominance. When governments run persistent deficits and rely on central bank financing (as Ghana did before the 2023 IMF programme), monetary policy loses its independence. The Bank of Ghana's measures included eliminating monetary financing of the budget as a structural benchmark under the IMF programme [1].

Exchange rate pass-through. In import-dependent economies, currency depreciation drives inflation regardless of the policy rate. Ghana's 27.8% Cedi depreciation in 2023 [8] overwhelmed any contractionary effect of higher interest rates. The Ministry of Finance acknowledged that the economy faces "tremendous pressure on the Cedi, creating an unfavourable balance of payments position" [25].

Wide interest rate spreads. Banks in Ghana and Nigeria maintain large spreads between deposit and lending rates, reflecting high operating costs, credit risk, and limited competition. The Ghana Association of Banks has documented how inflation and exchange rate movements transmit to bank lending behaviour, with transmission being incomplete and asymmetric [26].

Why Transmission Works in South Africa

Deep financial markets. South Africa's bond market, equity market, and banking sector are among the most developed in emerging markets. Government bond yields respond rapidly to SARB rate decisions, with the yield curve shifting 40-140 basis points in response to policy changes [22].

Institutional credibility. SARB's inflation targeting framework, operating since 2000, has built a track record that anchors expectations. National Treasury's strategic planning integrates monetary policy considerations, with macroeconomic policy and financial regulation operating as coordinated functions [27].

Banking sector pass-through. South African banks use prime as a reference rate directly linked to the repo rate [24]. When SARB moves the repo rate, commercial lending rates adjust within days. This is the most efficient transmission mechanism among the four countries.

The MPIF reform. The Monetary Policy Implementation Framework introduced in 2022 enhanced SARB's ability to manage structural liquidity and improve policy transmission [21]. The SARB has also studied monetary policy transmission dynamics from comparable economies, including the Bank of England's work on exchange rate and credit channels [28].

5. Country Profiles

Ghana: Crisis, Recovery, and the Limits of Monetary Policy

GDP (2024): $82 billion

The 2022-2023 crisis was a case study in transmission failure. With inflation at 54%, a depreciating currency, and sovereign debt distress, the Bank of Ghana raised rates aggressively but could not contain inflation because the primary driver was fiscal -- not monetary. The economy grew just 0.5% in 2020, and by 2022, the Cedi had depreciated from GH6/USD to GH14/USD [7].

The 2025 recovery demonstrates that monetary policy transmission can be restored when fiscal policy supports it. The IMF programme, which included a 5.1 percentage point fiscal consolidation over 2023-2026 [1], eliminated the fiscal dominance that was blocking transmission. By 2025, inflation had collapsed to 6.3%, treasury bill rates fell from 30% to 11%, and the Cedi appreciated 42.6% against the USD [5]. The establishment of the Ghana Gold Board and strong external reserves ($11.4 billion, covering 4.8 months of imports) provided the exchange rate anchor that monetary policy alone could not [29].

Transmission grade: C+ (improving). Transmission was effectively broken during 2022-2023 but has been substantially restored through fiscal consolidation and structural reform.

Nigeria: The Multiple Rate Distortion

GDP (2024): $252 billion (down from $647 billion in 2022 due to naira float)

The core problem in Nigeria is that monetary policy operated in a fundamentally distorted environment for nearly a decade. The CBN maintained multiple exchange rate windows (official, NAFEX, bureau de change, parallel) with spreads exceeding 100% [12]. This meant that the MPR -- the supposed anchor of the monetary system -- was setting a price in a market that did not exist. PwC's analysis of exchange rate dynamics shows the naira moving from approximately 305/USD (2020 official) to 800/USD (2024 post-float) [4].

The June 2023 naira float was the most important monetary policy event in Nigeria in a decade. By eliminating the artificial official rate, it exposed the true cost of imported goods and services, drove inflation to 26.72% [3], and caused USD-denominated GDP to plummet. The CBN's response was to keep tightening, taking the MPR to 18.75% by mid-2023 (its final step that year, from 18.5%) [3], with further increases expected.

Food inflation hit 33.2% year-on-year in late 2024, with the burden falling disproportionately on lower-income households. This is a transmission channel that works in reverse: tight monetary policy raises borrowing costs for agricultural producers, potentially exacerbating supply-side food inflation even as it tries to reduce demand-side pressure.

Pension fund impact. The National Pension Commission reported that rising MPR increased short-and-medium-term yields, benefiting pension fund returns but raising costs for government and corporate borrowers [11]. The Monetary Policy Rate concept in Nigeria has been described as the tool through which the CBN regulates economic activities and stabilizes the financial system, but its effectiveness depends on the credibility of the broader policy environment [30].

Transmission grade: D+. The naira float was a necessary precondition for functional transmission, but the economy is still adjusting. Transmission will remain impaired until exchange rate stability is established and inflation expectations are re-anchored.

Kenya: The Quiet Performer

GDP (2024): $120 billion

Kenya's monetary policy framework is less dramatic than Ghana's or Nigeria's, but arguably more effective. The CBK operates a CBR-based system with clear communication and a functioning interest rate corridor [14].

Transmission channels. The CBK explicitly identifies four channels: interest rate, credit, exchange rate, and asset price. Its presentation on the transmission mechanism notes that the CBR forms the base for all monetary policy operations and has enhanced clarity and certainty in monetary policy operations. However, effectiveness depends on the stability of the money demand function, which expanding financial services (including M-Pesa) have complicated [14].

The 2023-2024 tightening cycle. The CBK raised the CBR from 10.5% to 13.0% to anchor inflation expectations and address exchange rate pressures [19]. This is a standard response that works when the central bank has credibility -- and Kenya's CPI trajectory (257 vs 749 for Ghana) suggests it does.

Capital markets role. The Capital Markets Authority noted that East Africa recorded the highest real GDP growth rate of 5.6% in 2017 compared to the continent's average of 3.6%, reflecting sound macroeconomic policies and sensible policy frameworks [31]. Kenya's relatively developed equity and bond markets provide additional transmission channels that are absent in Ghana and Nigeria.

Transmission grade: B. Functional but constrained by limited financial depth outside Nairobi and the measurement challenges posed by mobile money innovation.

South Africa: The Transmission Benchmark

GDP (2024): $401 billion

South Africa's monetary policy transmission is the benchmark against which the other three should be measured. It is not perfect -- structural unemployment at 33%, loadshedding, and fiscal pressures all limit the real-economy impact of monetary policy -- but the institutional framework functions as designed.

The repo rate mechanism works through direct pass-through to the prime rate, which banks use as their reference for lending. When SARB adjusts the repo rate, the prime rate moves in lockstep, and lending rates across the economy adjust accordingly [24].

Bond market transmission. The government bond yield curve decreased by 40-140 basis points in the period under review, reflecting improved investor confidence, stronger emerging market demand, and improvements in the domestic political environment [22]. This yield curve response is itself evidence of effective transmission -- rate expectations are being priced by market participants who believe SARB's commitment to inflation targeting.

The fiscal coordination challenge. The Financial and Fiscal Commission has noted that while direct trade with Russia and Ukraine is limited, the war's impact on global trade complicates the role of monetary policy authorities in maintaining price stability without choking growth [32]. Rising domestic debt levels also risk crowding out private investment and limiting the effectiveness of rate cuts [33].

Transmission grade: A-. Near-textbook transmission through interest rate and credit channels, constrained by structural economic challenges (unemployment, inequality, energy insecurity) that limit the real-economy impact of monetary policy.

6. Policy Implications

For Ghana

The 2025 recovery demonstrates a template: fiscal consolidation first, then monetary policy can work. The primary surplus of 1.9% of GDP [5], the IMF programme discipline, and the establishment of the Ghana Gold Board for reserve accumulation created the conditions for monetary policy to transmit. The challenge is sustaining these gains through the political cycle. Ghana should institutionalise the prohibition on monetary financing and strengthen the BoG's operational independence.

For Nigeria

The naira float was necessary but not sufficient. Nigeria needs to establish a single, market-determined exchange rate and maintain it through credible monetary policy rather than administrative controls. The MPR of 18.75% against inflation above 26% still implies a deeply negative policy real rate (roughly −8% on a rate-minus-CPI basis). The CBN must signal -- and deliver -- a commitment to positive real rates before transmission can function.

For Kenya

Kenya's challenge is extending transmission beyond Nairobi. The CBK's framework works for the formal banking sector, but mobile money, SACCOs, and informal lending operate partially outside the transmission mechanism. The introduction of the 3-day repo [18] was a positive step toward improving short-term liquidity management and transmission efficiency.

For South Africa

SARB's challenge is maintaining credibility while dealing with structural constraints. The 8.25% repo rate with 5.3% inflation delivers a positive real rate, but the high prime rate (11.75%) creates affordability pressures for households and SMEs. The MPIF reform should continue to evolve to address growing structural liquidity [21].

Cross-Cutting

| Factor | GH | NG | KE | ZA |

|---|---|---|---|---|

| CPI multiplier (2010-2024) | 7.5x | 7.0x | 2.6x | 2.0x |

| Real interest rate (latest) | N/A | 2.9% | 7.8% | 7.4% |

| GDP (2024, USD) | $82B | $252B | $120B | $401B |

| Transmission grade | C+ | D+ | B | A- |

| Primary constraint | Fiscal dominance | Multiple FX rates | Financial depth | Structural unemployment |

Real interest rate = the World Bank real lending rate (FR.INR.RINR: lending rate minus the GDP deflator). On a policy-rate-minus-CPI basis, Nigeria's real rate is sharply negative (≈ −8%); the two gauges diverge, as discussed in §3.

7. Data Sources and Methodology

This report draws on 24 analytical queries to the KANA AI database and 33 citations from authoritative sources across all four countries. Quantitative data includes:

- Consumer Price Index (2010 = 100): 25 annual observations per country (2000-2024) from World Bank Development Indicators (FP.CPI.TOTL)

- Real interest rate (%): 24-25 annual observations per country (2000-2023/2024) from World Bank Development Indicators (FR.INR.RINR)

- GDP (current US$): 25 annual observations per country from World Bank Development Indicators (NY.GDP.MKTP.CD)

- Exchange rate (NGN/USD): 5 observations (2020-2024) from PwC Nigeria economic outlook

Qualitative analysis draws on primary sources including central bank communications, ministry of finance budget statements, pension commission reports, banking association research papers, and competition authority publications. All sources are classified by trust tier: T1 (government/statutory), T2 (regulatory bodies), and T3 (professional/research organisations).

Limitations

This analysis is descriptive and cross-country rather than a formal econometric estimation of monetary transmission. Three limitations bound the conclusions. First, real-interest-rate coverage is uneven across the four countries and study years, so cross-country comparisons of real rates are directional rather than exact. Second, the transmission discussion is qualitative — it traces how rate decisions move through inflation, the exchange rate, and the real economy, but does not estimate pass-through coefficients or impulse responses. Third, several headline relationships are anchored in the 2022–2024 crisis period; coefficients and co-movements observed under acute stress need not hold in a normal-rate regime. The figures should therefore be read as the structural pattern across these markets, not as a calibrated forecasting model.

8. References

- Ministry of Finance Ghana, "2023 Mid-Year Policy Review," [link]

- National Credit Regulator (South Africa), "NCR Annual Report 2024," [link]

- National Pension Commission (Nigeria), "Third Quarter Report 2023," [link]

- PwC Nigeria, "2025 Nigerian Budget and Economic Outlook," [link]

- Ministry of Finance Ghana, "Resetting Ghana's Economy: The 20 Reforms and Achievements That Defined 2025," [link]

- Ministry of Finance Ghana, "2023 Budget Highlights," [link]

- Ministry of Finance Ghana, "Ghana Medium Term Revenue Strategy 2024-2027," [link]

- Ministry of Finance Ghana, "2024 Mid-Year Fiscal Policy Review," [link]

- Ghana Association of Banks, "Interest Rates and Non-Performing Loans," [link]

- National Pension Commission (Nigeria), "2014 Annual Report," [link]

- National Pension Commission (Nigeria), "Q4 2022 Report," [link]

- PwC Nigeria, "Current Financial Reporting Issues: FX," [link]

- Nigeria Deposit Insurance Corporation, "Impact of Monetary Policy on Financial Openness in Nigeria," [link]

- Central Bank of Kenya, "Monetary Policy and the Transition Towards Inflation Targeting," [link]

- Central Bank of Kenya, "35th Monetary Policy Statement, December 2014," [link]

- Central Bank of Kenya, "Weekly Bulletin, July 2014," [link]

- Central Bank of Kenya, "Banking Circular No. 5 of 2015 -- Review of CBR," [link]

- Central Bank of Kenya, "Banking Circular No. 8 of 2015 -- Review of CBR and Introduction of 3-Day Repo," [link]

- National Treasury (Kenya), "2024 Budget Review and Outlook Paper," [link]

- Kenya Bankers Association, "Monetary Policy Risk-Taking Transmission Channel," [link]

- National Treasury (South Africa), "IMF Staff Report for 2025 Article IV Consultation," [link]

- National Treasury (South Africa), "Debt Management Report 2024-25," [link]

- PwC South Africa, "Major Banks Analysis March 2024," [link]

- Banking Association South Africa, "Statement on the Prime Interest Rate," [link]

- Ministry of Finance Ghana, "2023 Budget Highlights," [link]

- Ghana Association of Banks, "Inflation Dynamics and Cost of Credit," [link]

- National Treasury (South Africa), "Strategic Plan 2005-2008," [link]

- South African Reserve Bank, "Monetary Policy Transmission Presentation," [link]

- Ministry of Finance Ghana, "2025 Mid-Year Fiscal Policy Review," [link]

- Cowrywise, "The Concept of Monetary Policy Rate," [link]

- Capital Markets Authority (Kenya), "Capital Markets Annual Report 2018," [link]

- Financial and Fiscal Commission (South Africa), "Submission on Economic Impact of Russia-Ukraine Conflict," [link]

- Financial and Fiscal Commission (South Africa), "Domestic Debt Levels Analysis," [link]

Disclaimer. This report is produced by KANA AI for informational and educational purposes only. It does not constitute investment advice, a research recommendation, or an offer or solicitation to buy or sell any security, and it should not be the sole basis for any investment decision. Figures are computed from publicly available data and reported company fundamentals, which may be incomplete, delayed, or contain errors; valuation ratios reflect the latest available data and can lag fast-moving prices. Past performance is not indicative of future results. Readers should conduct their own due diligence and consult a licensed financial adviser. KANA AI accepts no liability for decisions taken on the basis of this report.

Next Step

Want to discuss this research or commission a similar analysis?

KANA AI can produce tailored research reports for your specific market, sector, or investment thesis.